Trading is stressful enough.....Your taxes shouldn't be! Ph: (813)746-8208

E-Mail: info@TraderTaxCoach.net

How Is It Taxed?

In a perfect world, all securities would be taxed the exact same. The reality is that the IRS taxes securities differently. In an attempt to bring some clarity to this issue, Trader Tax Coach has put together a brief explanation of how different types of securities are taxed.

First let's review the two different ways investments can be taxed:

Ordinary Income / Loss

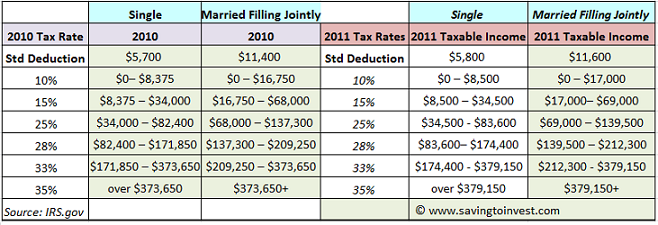

If a security is taxed as ordinary income it is subject to your marginal tax rates, depending on where you fall in the table below:

If you have an ordinary loss, it offsets any other income you may have dollar for dollar. For example, if you have a $10,000 ordinary loss, any other income you may have (W-2 job, spouse's income, etc) is decreased by $10,000. Ordinary losses are not subject to the $3000 annual limit that is imposed on capital losses (see below).

If you do not have any other income source, ordinary losses can generally be carried back 2 years by filing amended returns, or they can be carried forward up to 20 years.

Coach says, "If you want to first carry the loss forward, attach a statement to your timely filed return that you are electing to relinquish the entire carry back period. If you filed the return without electing to forgo the carry back period, you can still make such an election on an amended return filed within 6 months of the due date of the original return."

Capital Gain / Loss

If a security is treated as a capital gain, there are two different ways it could be taxed. Securities held less than a year will be treated as a short term capital gain. Most traders will fall into this category. Short term capital gains are taxed at your current marginal tax rates (the same as ordinary income). Those rates vary depending on the amount of your income. Please reference the table above to see the 2011 tax rates.

If you've held that security for over a year, the gain is treated as a long term capital gain and is taxed at the 15% level if you are in the 25% or higher income tax bracket (see the table above). If you are below the 25% income tax bracket, your long term capital gains rate is 0%!

If you experience a capital loss, you can use it to offset other capital gains dollar for dollar. If your capital losses exceed your capital gains, you can take a capital loss deduction. You are allowed to take up to a $3000 (or your total capital loss, which ever is less) against other income sources you may have. If your total capital loss is more than the $3000 limit, you can carry forward the excess to the next tax year. You can repeat this process until either it is completely used up.

Mark to Market Accounting

If you elect mark to market accounting for your trading business, it will effectively change the taxation of your capital gains / losses into ordinary gains / losses. There are advantages and disadvantages to making this change. For more information on mark to market accounting please click here.

Coach says, "If you are trading equities, options, or ETFs, it is a no brainer to elect the mark to market accounting method since your trading gains will be classified as short term capital gains and taxed as ordinary income by default. Plus, if you have losses, you are not subject to the $3000 capital loss rules!"